Materiality is a fundamental concept in auditing that helps auditors to determine the magnitude of discrepancies in financial statements that are significant enough to influence the decisions of users, such as investors, lenders, regulators, etc. In simple terms, it acts as a filter, allowing the audit to focus on what truly matters.

SA 320 – Materiality in Planning and Performing an Audit provides a structured approach for auditors to assess and apply materiality throughout the audit process. By setting appropriate materiality thresholds, auditors can effectively plan the scope and nature of their procedures, ensuring focused attention on areas of risk and significance. This enables the audit to be both efficient and impactful, supporting the objective of presenting financial statements that offer a true and fair view. Let us delve into the blog to explore the scope and application of SA 320 in greater detail.

I. A Step-by-Step Approach: From Benchmark to Judgement

The process of determining materiality under SA 320 involves several key steps that include:

A. Establish a Benchmark

Begin by selecting a Benchmark – a financial measure that represents the entity’s performance or size. The benchmark serves as the basis on which materiality is calculated. It is determined based on the nature of the entity and what users of the financial statements are likely to focus on:

For example:

- Profit Before Tax – suitable for profit-orientated entities,

- Total Revenue – suitable when revenue is the key performance indicator

- Total assets – relevant for asset-intensive businesses or non-profit organizations

B. Determine Materiality Thresholds

Apply a percentage to the chosen benchmark to set a threshold – above which misstatements are considered material. This threshold aids in audit strategy.

For example:

- 5% on Profit Before Tax of ₹10 crores results in an overall materiality of ₹50 lakhs.

C. Set Performance Materiality

Set a lower limit for determined materiality. This is done to be extra careful. It helps to make sure that small amounts do not add up to something big enough to mislead users of financial statements.

For example:

- If overall materiality is ₹50 lakhs, performance materiality might be set at ₹40 lakhs (80% of overall materiality), considering factors like the entity’s control environment and history of misstatements.

D. Specific materiality for Certain Classes of Transactions

Some transactions may require special consideration with respect to materiality during the process of auditing. Set special materiality thresholds for relevant classes of transactions, account balances or disclosures independently, without linking them to the overall materiality level.

For example:

- Key Management Personnel (KMP) compensation disclosures with a specific materiality threshold of ₹5 Lakhs, even if the overall materiality is much higher.

E. Revising Materiality During the Audit

Revise materiality levels on coming across new facts or changes in circumstances during the audit. This ensures that the judgements remain accurate, and the audit stays relevant.

For example:

- The auditor discovers that internal controls are weaker than initially thought and lowers the materiality threshold to increase testing and reduce the risk of missing important errors.

F. Documentation

Proper documentation ensures transparency and supports the auditor’s conclusions. Keep clear records of all materiality decisions, including:

- the chosen benchmark

- overall and specific materiality levels

- performance materiality

- any changes made during the audit.

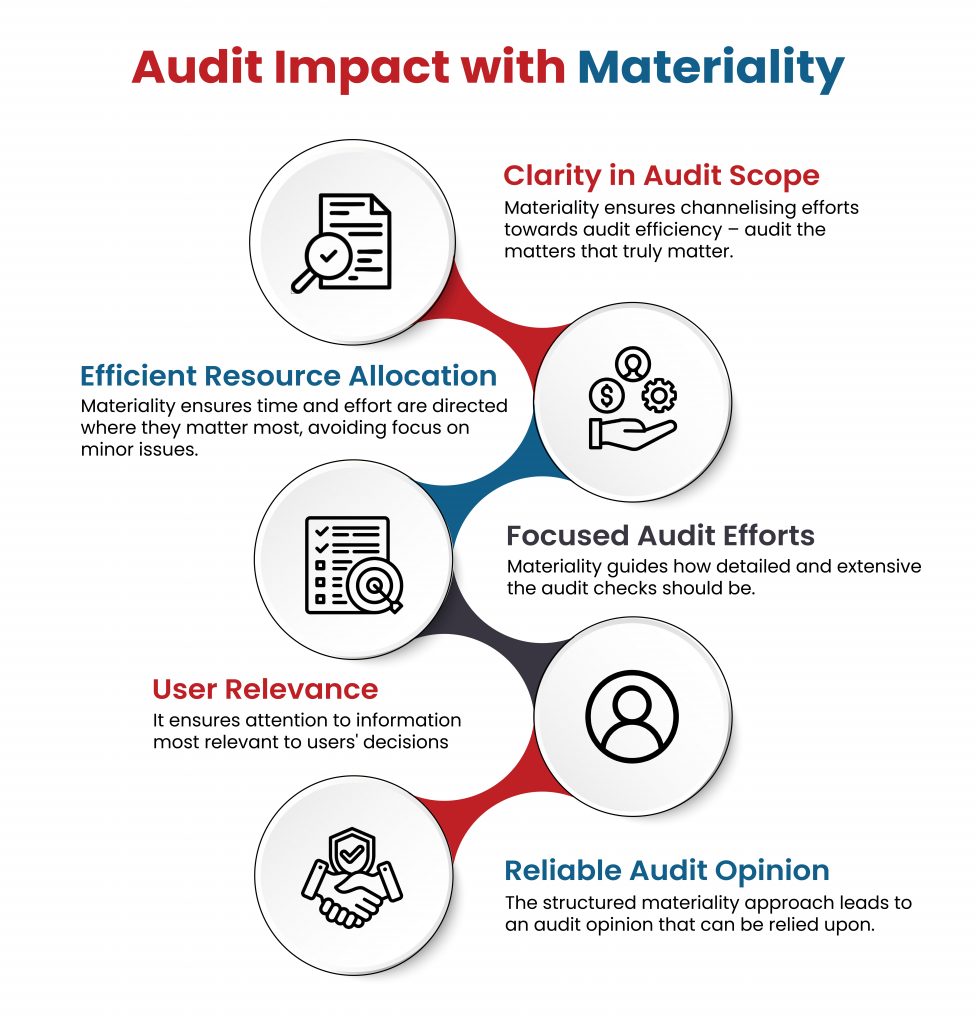

II. Audit Impact with Materiality

III. Conclusion

Materiality plays a vital role in shaping the direction, depth, and efficiency of an audit. However, determining materiality is not a one-size-fits-all formula. It requires professional judgement, considering the specific context, risks, and users of each entity’s financial statements. A well-applied materiality framework ensures that the audit remains both meaningful and impactful.

Contributors

CA N Srilatha Bhat – LinkedIn

Kuldeep Sarma – LinkedIn

Poonam Vernekar – LinkedIn